About the data coming in, Poole said:

It is rare that a single data report is decisive for the FOMC. The economic outlook is determined by numerous pieces of information. Important data such as the inflation and the employment reports are cross checked against other information. The FOMC is aware of possibility of data revisions and short-run anomalies.

My key point is that market commentary indicating that the FOMC is unpredictable is off base. Typically the FOMC cannot be predictable because new information driving policy adjustments is not predictable. All of us would like to be able to predict the future. We in the Fed do the best we can, but the markets should not complain that the FOMC lacks clairvoyance! What the FOMC strives to do is to respond systematically to the new information. There is considerable evidence that market does successfully predict FOMC responses to the available information at the time of regularly scheduled meetings

Followed by:

I myself do not finally make up my mind on my policy position until I’ve heard both staff presentations and the views of other FOMC participants. More accurately, I go into each FOMC meeting with a view on the appropriate policy action given my assessment of the economic outlook, but I try to be as open as I can to having my view altered by discussion at the FOMC meeting. There are certainly instances when I have changed the view I took into the meeting as a consequence of the discussion.

The employment number tomorrow will not push the Fed in one direction or the other. September is sit on your hands. The key aspect of tomorrow's employment report is that if the data are weak it sets up a probability that the Fed goes in October. If the data are neutral to strong, it will pretty much take October out of play as far any policy moves. Why? Because the Fed likes to have a few months of running data before declaring a trend change and reacting, barring some unforseen significant event (9/11 comes to mind). If Sep is weak and then Oct is weak, we have the beginning of something that the Fed might just react to.

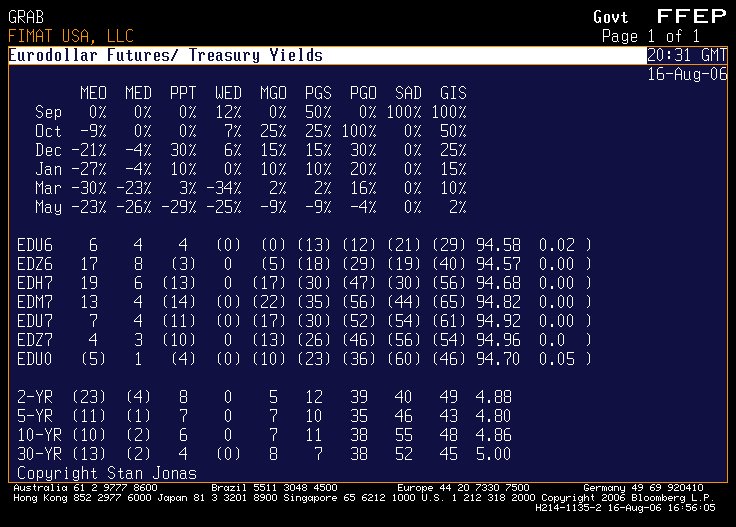

Market pricing is interesting. For October the market is giving a cumulative 7% chance that they do something -- 3% for an ease, 4% for a tightening. Chances of a move in December (remember that these probabilities accumulate across the months) -- 37%, 24% of tightening and 13% of an ease. In other words, the Fed has done its job. They have brought us to neutral and the Fed has the market evenly divided on what they do next.

Moving into next year, the market swings into the higher likelihood of an ease. Looking at the 94.625 call option in Dec Euros, the pricing suggests that there is a 30% chance of a Fed ease. Market is more sure about the future course of the economy than the Fed seems to be. This is what Poole is telling us -- they don't make policy on one number and they don't know today what they are going to do at the next meeting. Everyone is just guessing.