One key to the continued potential for growth, as I noted yesterday, is the credit creation process -- and it is alive and well. Yesterday's blog illustrated that commercial banks are still easing credit standards for commercial and household borrowers. This is not typical for a late cycle period with a marginally negative curve.

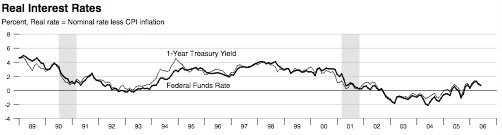

Add to the easy credit standards the fact that the cost of money is still low in real terms. The Federal Reserve of St. Louis just released its Monthly Monetary Trends. I have lifted from the publication their chart on real interest rates. Trust the calculation, this data find its way to the FOMC.

Most, however, are still nervous for the economy and believe that the Fed has gone too far. Some are even touting their higher odds for a recession next year. There is some reason to be nervous, but not because the Fed has been too restrictive. It is because of weakness in the demand for capital.

The Fed controls the cost of the supply (to an extent) but it can't make firms borrow. Firms aren't borrowing because money is too expensive, its because balance sheets are too leveraged. The economy is undergoing a hand off of growth leadership from housing to capex. Sometimes the ball gets dropped, sometimes not. Next several months tell the tale.

No comments:

Post a Comment