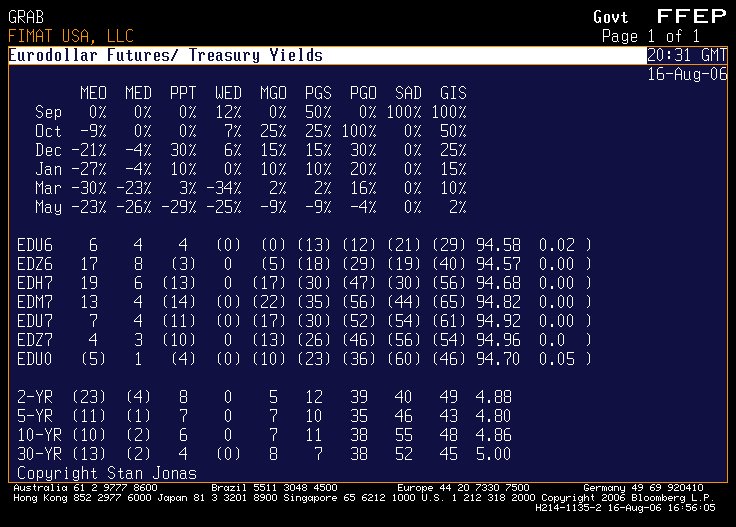

The WED column is the probabilities drawn from where the market closed. Note that there is still a cumulative 25% probability that the Fed tightens at some point this fall. Predictably, market sentiment has moved further by future eliminating tightenings and setting up the ease for next year. The cumulative ease is 50bp in 2007.

The other columns reflect different scenarios and the impact on Euros and coupon securities. For example, if we go back to where we were in probability space in the spring (GIS column), the 2-year would have a 49 basis point rise in yield. If we move toward a real ease scenario in term of expectations (MEO column), 2-year rallies 23 basis points. Once again, law being law, these are only references and guides and should not be taken as gospel truth, as the saying goes.

Where is the Fed as opposed to market sentiment? Steadier at the helm of expectations, for one thing. Market participants love to jump from one side of the boat to another with every data release. If the Fed acted that way the economy would be in real trouble. We have seen what happens when a fan (George Steinbrenner) runs a team as opposed to a professional (Brian Cashman/Joe Torre). There is no panic in professionals. Traders, like fans, are all about panic -- in the aggregate. To be fair it isn't really panic, it is the need to jump out ahead of everyone else in order to make money. The net effect, however, is that it looks like panic. The professionals, the Fed, will do nothing in Sep because it takes more than a data point or two to convince them that their expectations are wrong. Only possibility for Sep is if something implodes the economy in a way that an ease is necessary.

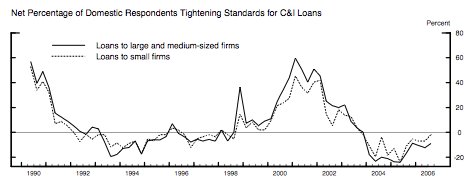

The economy is clearly moderating but, unlike some market seers, I do not see the wheels to coming off the U.S. economy. The next two charts from the Federal Reserve's Survey of Loan Officers reflects, in part, where my view is based. This chart below illustrates that commercial banks have been easing standards to their commercial borrowers. When the curve is inverted, lending standards tighten (the pattern of the line dovetails nicely with the slope of the Treasury curve). Now we have an inverted curve with more banks easing standards than tightening them. So when the Fed tells us that this time the curve's impact is different, the curve's impact IS different.

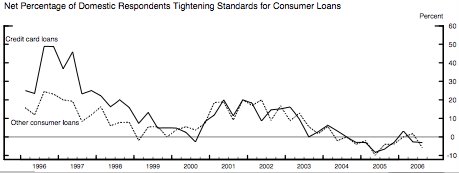

The chart below illustrates that with all the indebtedness of the household sector, banks aren't particularly concerned with household credit.

The point? Economies grow when credit expands. If the banking system shuts down, no country can grow -- be it Thailand, Zaire, England or the U.S. The U.S. banking system is healthy and willing to lend, more than willing as evidenced by their diminished credit standards. Further, the cost of money is still not high. U.S. growth is moderating, as the Fed noted. It is not heading into recession as long as this credit expansion is alive and well. The market pricing, especially for next year, is more bullish than it should be given the continued potential for growth. The market went overboard in its effective elimination of Fed tightenings past Sep and by emphatically pricing an ease in 2007. If you think I am wrong remember that the Fed likes to manage the fan's (er, market's) expectations. Read what just came out:

"If anybody tells you with absolute conviction that the Fed is done raising interest rates or with equal

conviction that they have only paused and will raise rates more starting

in September or October, remind yourself that at best -- and I'm being

generous here -- they are only guessing."

Fed's Fisher Sees'Definite Increase in Inflationary Momentum'>

2006-08-16 13:56 (New York)

1 comment:

Who knows where to download XRumer 5.0 Palladium?

Help, please. All recommend this program to effectively advertise on the Internet, this is the best program!

Post a Comment