In response to a question regarding the market's expectations of Fed policy next year, Poole gave an interesting resaponse. He noted that having the 10-year yielding 60 basis points under funds was not a tenable relationship for the long run. The trader, he added, is looking for less inflation and weaker growth and expecting the Fed to aggressively drop rates to a level below 4.65% (10-yr yield). Poole added that market forecasts, as honest and as good as they can be, do not have a good track record.

If inflation eases off, as the FOMC hopes, and real growth stays at or near potential, the Fed will not have to ease agressively and the 10-year yield would have to rise up to the funds rate or higher.

My italicized bold highlight informs us that IF the above scenario comes true, the FOMC is already set to give the market back the last 25 basis point hike.

In sum, if you think the Fed has done enough to quell inflation and not squash the economy, price in a 25bp cut for next year and short the 10-year. As for the timing of the move, considering that they want to see a solid pattern of data and are willing to wait until they get it, a March ease looks like the best bet.

Unless the unexpected occurs.

Friday, September 29, 2006

Neutral Is Neutral Is Neutral Until It Isn't

As I wrote last night, Bill Poole, President of the St. Louis Fed, was going to feed us what the Fed has been feeding us: The funds rate is at neutral until the data prove that it isn't. Between the lines, there is a bit of a wink to the expectations that an ease next year is not out of the question but he also lays out the parameters;

The italics are mine.

Where is the wink to an ease next year?

So the Fed isn't expecting an upturn anytime soon, and while they expect the economy to slow to a less than 3% real growth path (the new non-inflationary trend path), if the wheels come off the proverbial bus they will be on it quickly -- there is no gradualism on the downside

As for market thinking, Poole notes:

Is the market right?

When the market has been wrong, it is generally when:

According to Fed studies, 70% of the difference between the Eurodollar futures market forecast for rates six months out and where rates acutally end up is explained by "no one saw it coming". Remember that when street people write with rock-solid confidence what is going to happen next and what the Fed will do about it.

The market overreacts to every data point, it has to. The street only gets paid when money changes hands, so getting everyone on edge about the importance of the next data release is part of the drill. Remember when it was the money supply data on Thursday night? Remember money supply?

Anyway, the Fed, being professional has no panic, professionals never do, which is why Poole says:

As for my neutral is neutral until it isn't, Poole closes with:

That may be where the Fed is, but not the market. As I wrote yesterday, Poole was going to disappoint the market by telling the grand poobahs of market opinion that he isn't ready to ease. It was predictable, as is the market's reaction. The 2-year Treasury is currently up 3.5 basis points on the day, 5's are up 4.3bps, and 10s are 3.7bps. The movement reflects the red Euros being down 3 to 4 basis points.

Even with this back up, the market is still pricing in 25% chance of an ease in Jan, around 25% to 30% in Mar and 40% in May. Pretty high odds considering Poole's comments. If you own the 2-year Treasury you own those odds. To give a sense of the risk, if the expectations went to 0% the 2-yr would back up near 60 basis points in yield.

I am predicting nothing but expecting anything. Odds of an ease are better than they are for a tightening, but the market is just too sure for me that the economy will need lower rates to avoid recession. May turn out to be true, and the Giants might win the Super Bowl, but how much do you want to bet on the outcome?

If incoming economic indicators show that both output and inflation are rising above these forecasts, then in the absence of any other information we can expect that the FOMC will increase its target fed funds rate. On the other hand, if both output and inflation come in weaker than expected, we are unlikely to see further increases in the federal funds target; indeed, if economic weakness is pervasive enough the FOMC will at some point reduce the target funds rate.

The italics are mine.

Where is the wink to an ease next year?

If the economy comes in below the baseline forecast in coming quarters, the FOMC will have room to act as aggressively as required. I have no idea what scale of easing might be appropriate, for that will depend on the nature of the incoming information. Still, I believe forecasters should assign a relatively low probability to deep recession precisely because of the FOMC's demonstrated willingness to act aggressively as necessary.

So the Fed isn't expecting an upturn anytime soon, and while they expect the economy to slow to a less than 3% real growth path (the new non-inflationary trend path), if the wheels come off the proverbial bus they will be on it quickly -- there is no gradualism on the downside

As for market thinking, Poole notes:

The market's evaluation of the prospects for policy is revealed in the futures markets for federal funds and Eurodollar deposits. Current futures prices predict that the fed funds target is expected to begin moving down. . . . the market's expectation of future policy easing has been taking hold gradually since late June, say, in response to data on the real economy suggesting that real growth is slowing and inflation data suggesting that the worst may be over on that front.

Is the market right?

I want to underscore my earlier point about the limited accuracy of those forecasts. Some of the forecast misses have been pretty dramatic.

When the market has been wrong, it is generally when:

Both the FOMC and the markets were surprised by incoming information . . .

According to Fed studies, 70% of the difference between the Eurodollar futures market forecast for rates six months out and where rates acutally end up is explained by "no one saw it coming". Remember that when street people write with rock-solid confidence what is going to happen next and what the Fed will do about it.

The market overreacts to every data point, it has to. The street only gets paid when money changes hands, so getting everyone on edge about the importance of the next data release is part of the drill. Remember when it was the money supply data on Thursday night? Remember money supply?

Anyway, the Fed, being professional has no panic, professionals never do, which is why Poole says:

. . .it is rare that a single data report is decisive. The economic outlook is determined by numerous pieces of information. Important data such as the inflation and the employment reports are cross checked against other information. . . .

. . . .Policymakers piece together a picture of the economy from a variety of data, including anecdotal observations. When the various observations fit together to provide a coherent picture, the Fed can adjust the intended rate with some confidence.

As for my neutral is neutral until it isn't, Poole closes with:

That the policy setting is data dependent is a good sign. It means that policy is in a range than can be considered neutral that is, thought to be consistent with the Fed's longer-run policy objectives. . . . I believe that is just about exactly where we are today.

That may be where the Fed is, but not the market. As I wrote yesterday, Poole was going to disappoint the market by telling the grand poobahs of market opinion that he isn't ready to ease. It was predictable, as is the market's reaction. The 2-year Treasury is currently up 3.5 basis points on the day, 5's are up 4.3bps, and 10s are 3.7bps. The movement reflects the red Euros being down 3 to 4 basis points.

Even with this back up, the market is still pricing in 25% chance of an ease in Jan, around 25% to 30% in Mar and 40% in May. Pretty high odds considering Poole's comments. If you own the 2-year Treasury you own those odds. To give a sense of the risk, if the expectations went to 0% the 2-yr would back up near 60 basis points in yield.

I am predicting nothing but expecting anything. Odds of an ease are better than they are for a tightening, but the market is just too sure for me that the economy will need lower rates to avoid recession. May turn out to be true, and the Giants might win the Super Bowl, but how much do you want to bet on the outcome?

Thursday, September 28, 2006

Poole Reconfirms Tomorrow What Market Refuses To Believe

William Poole, the official unofficial spokesman for the FOMC speaks tomorrow at Middle Tenessee State University on U.S. Data Dependency. I am not sure what that means but I am sure that his talk or post-talk q&a will reiterate what the Fed has been saying since Bernanke's testimony in July -- neutral is neutral is neutral until it isn't and the data hasn't convinced the Fed otherwise.

Ever since the Fed met on September 20, the market has taken weaker activity around Philadelphia, softness in housing, and falling oil prices to mean that the Fed has a 15% shot of easing in December and almost certainty that the Fed eases sometime between now and May.

Poole tomorrow lets everyone know that the adults are back in charge. I can not see what data have been released to shift him from the view that rates are high enough to slow but not kill the economy, slow housing down to the pace where it should be given the level of income and employment growth, and therefore slowly ease inflation back down. He and the heads of the Dallas and Richmond Feds seem not to be as concerned with the slowdown as the market and they aren't the only ones.

Earlier this week, the real adults, Volcker and some of the other previous heads of the NY Fed had a discussion at the Women's Economic Round Table in New York.

Here, lifted from the Bloomberg article written by reporter Craig Torres, are some comments to focus on:

We shall see what he says just before the ISM number (Chicago is reported tomorrow, national on Monday) and employment in a week. He won't say they are ready to ease, only that aren't going to be tightening. That should be enough to disappoint.

Ever since the Fed met on September 20, the market has taken weaker activity around Philadelphia, softness in housing, and falling oil prices to mean that the Fed has a 15% shot of easing in December and almost certainty that the Fed eases sometime between now and May.

Poole tomorrow lets everyone know that the adults are back in charge. I can not see what data have been released to shift him from the view that rates are high enough to slow but not kill the economy, slow housing down to the pace where it should be given the level of income and employment growth, and therefore slowly ease inflation back down. He and the heads of the Dallas and Richmond Feds seem not to be as concerned with the slowdown as the market and they aren't the only ones.

Earlier this week, the real adults, Volcker and some of the other previous heads of the NY Fed had a discussion at the Women's Economic Round Table in New York.

Here, lifted from the Bloomberg article written by reporter Craig Torres, are some comments to focus on:

``I am a little bit more worried about inflation,'' said Volcker, 79, speaking at a discussion sponsored by the Women's Economic Round Table in New York yesterday. Gerald Corrigan, who served as New York Fed president from 1985 to 1993, said he shared Volcker's concerns.That is the what Poole and Bernanke and their compadres are concerned about -- the 3 year mountain of liquidity that Greenspan left them. They are not worried about housing and, as per Poole's comments on Bloomberg earlier this month, the drop in oil prices and bond yields are a stabilizer for the economy.

While the inflation rate isn't ``high'' or ``running away,'' Volcker said, ``it is kind of creeping up, and I am impressed by the degree of pressure, if that is the right word -- psychological pressure, political pressure -- there is not to do anything about it.''

We shall see what he says just before the ISM number (Chicago is reported tomorrow, national on Monday) and employment in a week. He won't say they are ready to ease, only that aren't going to be tightening. That should be enough to disappoint.

Friday, September 22, 2006

Greenspan Puts ...... Again

Rumor in the market today was that Greenspan told a hedge fund group that the Fed was not concerned about inflation and would inject liquidity into the system if the housing slump turned serious. Serious is in the eye of who is slumping (the next town, the neighbor, or me), and how much liquidity is enough to combat the slump. If it were serious, history has proven it would be more than a 25 bp drop.

Earlier this year, Greenspan gave a private talk that became public when he said the Fed would pause by June and then start easing about 6 months later to stem the weakness in housing.

Since that scenario has played out thus far, it is tough to ignore the rumored comments. The bid/offer for an ease by December is 14/24 after settling at 12 yesterday (Dec Fed funds digitals). The puts are still trading at 6.

How ready is Bernanke et al ready to jump in and ease to save people who took the housing boom a bit too seriously in terms of financial leverage?

During the 90s one of the mantras feeding the equity market was the perceived Greenspan put. That is, he would ease if the market faltered thereby removing downside risk. It is not clear to me that the current group sitting around the FOMC table every six weeks is of the mindset to create a free put on housing for real estate speculators. For one thing, jumping in so quickly puts a floor on inflation, which at least the Richmond Fed is still concerned about, and an ease now does nothing to solve the negative saving rate problem.

I am still of the mindset that rates are low enough, general economic momentum strong enough (now bouyed a bit by lower energy prices and lower yields) that the economy will exhibit enough growth to keep the Fed exactly where it is.

The upcoming employment data will again be important. Signs of weakness there would push the Fed towards an ease before year end. Another 125,000 number, 5.25% as far as the eye can see --- or at least till the following month's data.

Earlier this year, Greenspan gave a private talk that became public when he said the Fed would pause by June and then start easing about 6 months later to stem the weakness in housing.

Since that scenario has played out thus far, it is tough to ignore the rumored comments. The bid/offer for an ease by December is 14/24 after settling at 12 yesterday (Dec Fed funds digitals). The puts are still trading at 6.

How ready is Bernanke et al ready to jump in and ease to save people who took the housing boom a bit too seriously in terms of financial leverage?

During the 90s one of the mantras feeding the equity market was the perceived Greenspan put. That is, he would ease if the market faltered thereby removing downside risk. It is not clear to me that the current group sitting around the FOMC table every six weeks is of the mindset to create a free put on housing for real estate speculators. For one thing, jumping in so quickly puts a floor on inflation, which at least the Richmond Fed is still concerned about, and an ease now does nothing to solve the negative saving rate problem.

I am still of the mindset that rates are low enough, general economic momentum strong enough (now bouyed a bit by lower energy prices and lower yields) that the economy will exhibit enough growth to keep the Fed exactly where it is.

The upcoming employment data will again be important. Signs of weakness there would push the Fed towards an ease before year end. Another 125,000 number, 5.25% as far as the eye can see --- or at least till the following month's data.

Wednesday, September 20, 2006

Where We Are Now

Fed statments be damned, the market remains undeterred in its quest to price in an ease next year. Spurred by softer data and ignoring the FOMC mantra to wait and watch, the traders and investors whose money flows determine fixed income prices pushed the probability of a 25bp ease by May of 2007 to near certainty. It seems that the whole course of the economy is now determined by manufacturing in the geography covered by the Philadelphia Fed. That might be true, and housing may be causing the economy to implode like a cheap tract house in Arizona, or it could be some wishful thinking on the part of market participants growing weary of negative carry.

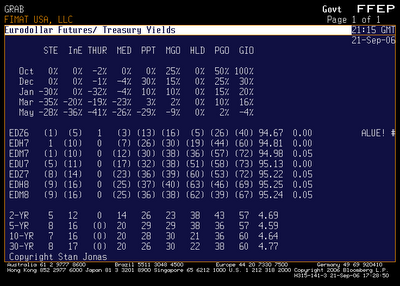

Here below is the current state of probability affairs as lifted from the Bloomberg page set out by my partner, Stan Jonas, and used to help feed the trading strategies of our fund (this is not a solicitation, etc, etc, etc, merely full disclosure on my part)

The interesting point here is the Thur column which lays out the probablities implied by current pricing. The market is setting the odds at 1 in 3 of a cut in January, 1 in 5 in Mar and 2 in 5 by May. Cumulatively it adds to certainty by the May meeting.

As for expectations between now and year end, the no change view has gone from 66% to 82%. In that 18% betting on one move or another, it was 2 to 1 or 3 to 2 in favor of a tightening. Today it swung the other way and sits at 2 to 1 in favor of an ease: 12% to 6%. These numbers are garnered from the Fed funds digital options that trade on the CBOT.

It seems that once the Fed stops, the market just has to believe the next move is an ease. History favors this view, no doubt, but when everyone sees it, something else suprises. The only real indicator to me that the economy is slowing is the drop in oil to $60/bbl. Since I believed growth and not a contrived shortage was driving the price up, I have to remain consistent in my logic.

There is, however, another aspect to lower yields and reduced oil prices. They are in and of themselves a buffer to weaker growth. Knowing this, the Fed shows no inclination to micro-manage the economy by changing rates 25bp from neutral (where we are now). With Fed funds neither constraining or subsidizing growth in the aggregate, the Fed seems perfectly content to let the economy fluctuate around some trend path, pushed and pulled by shifts in relative prices. Let market participants draw strong trends from single data points, the Fed will have none of that in its own decision making process.

The Fed is out of the way, the bigger disappointment to the market will not be that they have tightened too much but that they did just enough.

Here below is the current state of probability affairs as lifted from the Bloomberg page set out by my partner, Stan Jonas, and used to help feed the trading strategies of our fund (this is not a solicitation, etc, etc, etc, merely full disclosure on my part)

The interesting point here is the Thur column which lays out the probablities implied by current pricing. The market is setting the odds at 1 in 3 of a cut in January, 1 in 5 in Mar and 2 in 5 by May. Cumulatively it adds to certainty by the May meeting.

As for expectations between now and year end, the no change view has gone from 66% to 82%. In that 18% betting on one move or another, it was 2 to 1 or 3 to 2 in favor of a tightening. Today it swung the other way and sits at 2 to 1 in favor of an ease: 12% to 6%. These numbers are garnered from the Fed funds digital options that trade on the CBOT.

It seems that once the Fed stops, the market just has to believe the next move is an ease. History favors this view, no doubt, but when everyone sees it, something else suprises. The only real indicator to me that the economy is slowing is the drop in oil to $60/bbl. Since I believed growth and not a contrived shortage was driving the price up, I have to remain consistent in my logic.

There is, however, another aspect to lower yields and reduced oil prices. They are in and of themselves a buffer to weaker growth. Knowing this, the Fed shows no inclination to micro-manage the economy by changing rates 25bp from neutral (where we are now). With Fed funds neither constraining or subsidizing growth in the aggregate, the Fed seems perfectly content to let the economy fluctuate around some trend path, pushed and pulled by shifts in relative prices. Let market participants draw strong trends from single data points, the Fed will have none of that in its own decision making process.

The Fed is out of the way, the bigger disappointment to the market will not be that they have tightened too much but that they did just enough.

Monday, September 18, 2006

Fed Tells Ip What They Have Fed The Market ...... and something more

In the Saturday Wall Street Journal, Greg Ip, the erstwhile journalist and relayer of unattributed Fed thoughts to the masses (at least the masses that read the WSJ), wrote an interesting piece entitled "Outlook Divides The Fed, The Street" (I didn't bother with a link since you need a subscription to access the article online).

The article contained some points of interest. For one, there is this:

In other words, don't expect anything in Sep or Oct or probably even Dec, since the Fed digests a flow of information before it decides to raise, lower, or hold. As of now, the information flow suggests that standing pat is the right stance.

The second message of this paragraph and one noted in this blog for at least the past month is -- "What is the market doing pricing an ease into next year?"

As Ip explains, the market is more pessimistic on growth than the Fed because they are more pessimistic on the impact of weak housing. Given the track record, it is better to bet on the Fed in a stakes race than on the "street". If you own a two-year Treasury, understand that the underlying bet is the flip -- against the Fed and with the street analysts/economists/etc. These street people are the same ones who told us last year that 3.5% was the neutral top and anything higher risks doom, destruction, and depression. The market, by the way, was forecasting a decline in the funds rate in 2006. As Casey Stengel used to say, "you can look it up"

Another thought is that while the bond market is trading at low yields reflective of the expectation for a Fed ease next year the stock market is doing very well, credit spreads are tight, and lending standards are easy. This combination is a recipe for expansion not contraction. Your money, your bet, your risk.

This line in the Ip article strikes me the most:

When did this happen?

The whole rationale behind the Greenspan policy in the mid 90s and the "new economy" paradigm, etc., etc., etc., was that high productivity, global sourcing, technological advances, and capital deepening meant that the economy could handle a much faster rate of growth and resource utilization without triggering inflation. Now it can't?

Some explanation is in order.

Is the explanation that the good fortune on inflation in the 90s was as much because of external forces, such as bad policy holding down Japan, as it was because of intended domestic policy (monetary and fiscal) and policy with unintended effects (the peace dividend)? And if outside forces effected domestic inflation to the extent that the Fed went from new paradigm to old inside of one business cycle, how can the Fed run a long-term policy based on inflation targetting when inflation is not totally the result of our doing?

These are the more important questions than what the Fed does this week and what it says after its done nothing.

The article contained some points of interest. For one, there is this:

"Recent speeches by Fed officials suggest that while they are willing to stay on hold for now to see if their forecast of slowing growth and falling inflation comes about, they do not share the pessimism on growth, or the optimism on inflation, implicit in expectations of a rate cut by mid-2007."

In other words, don't expect anything in Sep or Oct or probably even Dec, since the Fed digests a flow of information before it decides to raise, lower, or hold. As of now, the information flow suggests that standing pat is the right stance.

The second message of this paragraph and one noted in this blog for at least the past month is -- "What is the market doing pricing an ease into next year?"

As Ip explains, the market is more pessimistic on growth than the Fed because they are more pessimistic on the impact of weak housing. Given the track record, it is better to bet on the Fed in a stakes race than on the "street". If you own a two-year Treasury, understand that the underlying bet is the flip -- against the Fed and with the street analysts/economists/etc. These street people are the same ones who told us last year that 3.5% was the neutral top and anything higher risks doom, destruction, and depression. The market, by the way, was forecasting a decline in the funds rate in 2006. As Casey Stengel used to say, "you can look it up"

Another thought is that while the bond market is trading at low yields reflective of the expectation for a Fed ease next year the stock market is doing very well, credit spreads are tight, and lending standards are easy. This combination is a recipe for expansion not contraction. Your money, your bet, your risk.

This line in the Ip article strikes me the most:

"Moreover, the Fed seems to think the economy's potential growth -- what it can achieve without straining business and labor capacity and thus fueling inflation -- is lower than many on Wall Street think."

When did this happen?

The whole rationale behind the Greenspan policy in the mid 90s and the "new economy" paradigm, etc., etc., etc., was that high productivity, global sourcing, technological advances, and capital deepening meant that the economy could handle a much faster rate of growth and resource utilization without triggering inflation. Now it can't?

Some explanation is in order.

Is the explanation that the good fortune on inflation in the 90s was as much because of external forces, such as bad policy holding down Japan, as it was because of intended domestic policy (monetary and fiscal) and policy with unintended effects (the peace dividend)? And if outside forces effected domestic inflation to the extent that the Fed went from new paradigm to old inside of one business cycle, how can the Fed run a long-term policy based on inflation targetting when inflation is not totally the result of our doing?

These are the more important questions than what the Fed does this week and what it says after its done nothing.

Thursday, September 14, 2006

Fed Tells Berry That It Wants To Tell Us More.......Or Less

Odd logic this is, for the Fed to go through one of its journalists to let us know that they want to "cast more light on the central bank's inner workings". They could've just told us directly, but I guess old habits are hard to break.

The article written by John Berry, on Bloomberg News on Thursday Sep 14, starts out with:

The article goes on to tell us:

This isn't about clarity, this is about keeping everyone's eyes on the horizon instead of their driving. They can ask us to do that because they have us convinced that they are the designated driver of choice.

As for what horizon we are driving towards, the article offers this (bold is mine):

This is all about about inflation targetting. An idea that, like many in economics, is wonderful in theory but somewhat problematic in the real world. Everyone understands that a low, stable, and predictable inflation rate induces business confidence to invest which, in turn, raises employment levels (the other one of the Fed's dual goals). This logic, right or wrong, is required because one policy lever can only work on one policy objective. Since the Fed works through the financial side of the economy, inflation has to be the target.

Take a look at growth, inflation, and the funds rate:

It easy to see that in the mid 90s similar real growth created far less inflation than we have today. Then, the Federal funds rate was significantly higher on its own and in relation to nominal GDP growth (add GDP and deflator). One could conclude that there is an overhang of monetary expansion still in the system since it was only this year that the funds rate got to the mid 90s level. Yet Fed officials talk about the tightening in the pipeline, as if rates have risen to some confiscatory level. My guess is that they are really talking about engineering a soft landing for housing now that the housing industry's rate subsidy is gone.

But the end of a subsidy doesn't mean rates are too high. There is nothing about the level of rates today to suggest anything other than that rates have, after two years, finally reached neutral. When did the economy become so rate sensitive that this level of rates risks recession? The market, in its infinite wisom, seems to think so. I think otherwise.

As for inflation and setting a target, the higher inflation today suggests a higher funds rate than prevailed in the mid 90s. Or, perhaps the funds rate was too high in the 90s, hence the idea that a 5+% rate will bring down current inflation. Or perhaps the answer is that the good inflation data of the 90s reflected the pace of growth of the G-10 nations -- most notably Japan. Those growth levels, lower then than now, directly effected commodity prices, namely oil. Therefore, then the Fed could afford to allow the economy to run at full steam without raising rates. The upshot is how do you pick a relevant inflation rate to target. Economics is one thing, policy is another.

The article written by John Berry, on Bloomberg News on Thursday Sep 14, starts out with:

Federal Reserve officials want to cast more light on the central bank's inner workings to give the public a better understanding of what they are doing and why. The big hurdle is figuring out how to go about it.

The article goes on to tell us:

The most important consideration, according to the minutes, was how to convey the FOMC's goals and Fed appraisals of where the economy is headed.

Fed Chairman Ben S. Bernanke has some ideas about how to lift the veil a bit more: He wants the committee to adopt a formal inflation goal and publish more frequent economic forecasts that would show the expected path for inflation.

This isn't about clarity, this is about keeping everyone's eyes on the horizon instead of their driving. They can ask us to do that because they have us convinced that they are the designated driver of choice.

As for what horizon we are driving towards, the article offers this (bold is mine):

More recently, the committee has indicated a willingness to take as long as two years to bring core inflation back down to 2 percent from the 2.4 percent increase for the 12 months ended in July.

This is all about about inflation targetting. An idea that, like many in economics, is wonderful in theory but somewhat problematic in the real world. Everyone understands that a low, stable, and predictable inflation rate induces business confidence to invest which, in turn, raises employment levels (the other one of the Fed's dual goals). This logic, right or wrong, is required because one policy lever can only work on one policy objective. Since the Fed works through the financial side of the economy, inflation has to be the target.

Take a look at growth, inflation, and the funds rate:

It easy to see that in the mid 90s similar real growth created far less inflation than we have today. Then, the Federal funds rate was significantly higher on its own and in relation to nominal GDP growth (add GDP and deflator). One could conclude that there is an overhang of monetary expansion still in the system since it was only this year that the funds rate got to the mid 90s level. Yet Fed officials talk about the tightening in the pipeline, as if rates have risen to some confiscatory level. My guess is that they are really talking about engineering a soft landing for housing now that the housing industry's rate subsidy is gone.

But the end of a subsidy doesn't mean rates are too high. There is nothing about the level of rates today to suggest anything other than that rates have, after two years, finally reached neutral. When did the economy become so rate sensitive that this level of rates risks recession? The market, in its infinite wisom, seems to think so. I think otherwise.

As for inflation and setting a target, the higher inflation today suggests a higher funds rate than prevailed in the mid 90s. Or, perhaps the funds rate was too high in the 90s, hence the idea that a 5+% rate will bring down current inflation. Or perhaps the answer is that the good inflation data of the 90s reflected the pace of growth of the G-10 nations -- most notably Japan. Those growth levels, lower then than now, directly effected commodity prices, namely oil. Therefore, then the Fed could afford to allow the economy to run at full steam without raising rates. The upshot is how do you pick a relevant inflation rate to target. Economics is one thing, policy is another.

Thursday, September 07, 2006

Yellen Back In The Poole; Mishkin's Paper Is The New Playbook

Janet Yellen, President of the Federal Reserve Bank of San Francisco, gave a speech in Boise (she must be walking back from Jackson Hole)to a Community Outreach Luncheon on "Prospects for the U.S. Economy" Just as at the end of July, Yellen essentially parroted Bill Poole's (President of the St. Louis Fed) recent speech and his comments the other day on the Bloomberg. In sum, the Fed has reached the neutral rate we were guessing about once the funds rate began its climb from 1% in 1/4 point steps beginning with the June 04 meeting. With Yellen having spoken the same speech as Poole, both sides of the FOMC debate (the sides that matter) are on the same page. Neutral is neutral is neutral until the data prove it isn't.

Markets, being creatures of habit, are having a difficult time with neutral because they can't get used to the Fed making us guess the next move rather than telegraphing it.

To understand what the Fed is communicating, leaving aside whether 5.25% is right or wrong, Prof. Frederick S. Mishkin (now a FOMC member) essentially wrote the "playbook" in his paper "Can Central Bank Transparency Go Too Far". Parsing the abstract alone underscores my point.

As for what the Fed was doing when it was telegraphing the long, steady climb from extraordinary ease to neutrality:

He later adds:

Compare this with the end of Yellen's speech today:

Getting back to Mishkin's paper:

Yesterday, Poole told us that future policy moves will be determined by future data that is unknown and unpredictable. Hence, it is impossible to know what the Fed will be doing next month let alone next year. Of course, he adds, ala the Mishkin prescription, that he will keep the funds rate high enough to keep inflation down.

Neutral is neutral is neutral until the data prove that it isn't.

The market still has a tiny bias that the Fed might tighten one more time this year. The December Fed funds digital options indicate a 33% chance that the Fed does something between now and the December 12 meeting with a bias (21 to 12) that the move is a hike in rates. Compared to a few trading days ago, the expectation that the Fed does nothing has risen from 60% to 67%. When the view was 60% the mix of the remaining 40% was dead even.

Looking at the market's pricing for next year, the leaning is still towards an ease, although less so. My guess is that the market is now at 40% certainty of a 100bp cumulative drop next year compared to 50% at the end of last week. The market is setting the odds of a bit better than 1 in 4 that the first drop occurs at the January 2007 meeting.

From my rudimentary calculations, if the market expectations shifted to 0% chance of any Fed actions from today on out, the yield on 2-year Treasurys would rise around 25 basis points. On the other hand, if the market prices 0% this year and gets a bit more aggressive on the ease picture for next year, the 2-year drops around 10 basis points in yield.

The risk is yours to figure based on your view of the world. But remember, the people running the world (the market world) are telling you that they don't know what is going to happen so they don't know what they are going to do. Pricing anything other than "no move" is just a guess.

Markets, being creatures of habit, are having a difficult time with neutral because they can't get used to the Fed making us guess the next move rather than telegraphing it.

To understand what the Fed is communicating, leaving aside whether 5.25% is right or wrong, Prof. Frederick S. Mishkin (now a FOMC member) essentially wrote the "playbook" in his paper "Can Central Bank Transparency Go Too Far". Parsing the abstract alone underscores my point.

As for what the Fed was doing when it was telegraphing the long, steady climb from extraordinary ease to neutrality:

Transparency is beneficial only when it serves to simplify communication with the public and helps generate support for central banks to conduct monetary policy optimally with an appropriate focus on long-run objectives.

He later adds:

Transparency can indeed go too far. However, central banks can improve transparency in discussing that they do care about reducing output fluctuations ... by emphasizing that monetary policy will be just as vigilant in preventing inflation from falling too low as it is from preventing it from being too high.... central banks can show that they do care about output fluctuations.

Compare this with the end of Yellen's speech today:

....while giving due consideration to the risks to economic activity....

..... policy must be responsive to the data as it emerges..... any additional firming should depend on how emerging developments affect the economic outlook....

The bottom line is this....... By pausing, we allowed ourselves more time to observe the data and more time to gauge how much, if any, additional firming is needed to pursue our dual mandate.

Getting back to Mishkin's paper:

These steps to improve transparency will increase support for the central bank's policies and independence, but avoid a focus on the short run that could interfere with the ability of the central bank to do its job effectively.

Yesterday, Poole told us that future policy moves will be determined by future data that is unknown and unpredictable. Hence, it is impossible to know what the Fed will be doing next month let alone next year. Of course, he adds, ala the Mishkin prescription, that he will keep the funds rate high enough to keep inflation down.

Neutral is neutral is neutral until the data prove that it isn't.

The market still has a tiny bias that the Fed might tighten one more time this year. The December Fed funds digital options indicate a 33% chance that the Fed does something between now and the December 12 meeting with a bias (21 to 12) that the move is a hike in rates. Compared to a few trading days ago, the expectation that the Fed does nothing has risen from 60% to 67%. When the view was 60% the mix of the remaining 40% was dead even.

Looking at the market's pricing for next year, the leaning is still towards an ease, although less so. My guess is that the market is now at 40% certainty of a 100bp cumulative drop next year compared to 50% at the end of last week. The market is setting the odds of a bit better than 1 in 4 that the first drop occurs at the January 2007 meeting.

From my rudimentary calculations, if the market expectations shifted to 0% chance of any Fed actions from today on out, the yield on 2-year Treasurys would rise around 25 basis points. On the other hand, if the market prices 0% this year and gets a bit more aggressive on the ease picture for next year, the 2-year drops around 10 basis points in yield.

The risk is yours to figure based on your view of the world. But remember, the people running the world (the market world) are telling you that they don't know what is going to happen so they don't know what they are going to do. Pricing anything other than "no move" is just a guess.

Tuesday, September 05, 2006

Poole On Bloomberg Tells Us All We Need To Know

Poole had a q & a on Bloomberg this morning, and if anyone was uncertain as to where the Fed is and, more important, where it is going to be, he ended all speculation.

Here are some of my highlights from his comments --

On housing and its impact on growth: There are always worry warts, on both sides. Housing is slowing. Fed expected it to slow. Fed wanted it to slow. Slowdown may be a bit more than expected but commercial construction is up and hires the same resources (labor and material) residential construction uses. Further, the employment data indicate an economy growing at potential. No reason to expect cascading weakness from housing to create a much slower economy.

Yield curve and market's forecast of Fed action: Negative curve can be viewed as anticipation of a Fed ease but lower bond yields are also a built-in stabilizer to the economy that helps housing and keeps the economy from getting weaker. As a predictor, curve has given false signals and the bond market is trying to predict policy action that will be driven by new information that, by definition, is random and unpredictable.

A key comment: Looking at a 6 month horizon, 70% of the fluctuation in the bond market comes from new, unanticipated information. New information is random, unpredictable, and policy is driven by new information.......

Summing up: Policy is as tight as it has to be and the economy is growing at potential. As such, inflation should moderate over time and the Fed can be patient and wait months even quarters, no reason to create a disturbance in the economy by changing the funds rate. Fed policy will be driven by new information that is viewed in context with all other information. New information is random and unpredictable. By extension, what the Fed will do in the future is unpredictable.

Meaning: Fed is done. Next policy move can be either way, although there is bias in the logic to presume that the suprise to cause the Fed to act will be indications of a weak economy. As for the timing of the next move --it might be a while, there is no hurry to do anything.

Here are some of my highlights from his comments --

On housing and its impact on growth: There are always worry warts, on both sides. Housing is slowing. Fed expected it to slow. Fed wanted it to slow. Slowdown may be a bit more than expected but commercial construction is up and hires the same resources (labor and material) residential construction uses. Further, the employment data indicate an economy growing at potential. No reason to expect cascading weakness from housing to create a much slower economy.

Yield curve and market's forecast of Fed action: Negative curve can be viewed as anticipation of a Fed ease but lower bond yields are also a built-in stabilizer to the economy that helps housing and keeps the economy from getting weaker. As a predictor, curve has given false signals and the bond market is trying to predict policy action that will be driven by new information that, by definition, is random and unpredictable.

A key comment: Looking at a 6 month horizon, 70% of the fluctuation in the bond market comes from new, unanticipated information. New information is random, unpredictable, and policy is driven by new information.......

Summing up: Policy is as tight as it has to be and the economy is growing at potential. As such, inflation should moderate over time and the Fed can be patient and wait months even quarters, no reason to create a disturbance in the economy by changing the funds rate. Fed policy will be driven by new information that is viewed in context with all other information. New information is random and unpredictable. By extension, what the Fed will do in the future is unpredictable.

Meaning: Fed is done. Next policy move can be either way, although there is bias in the logic to presume that the suprise to cause the Fed to act will be indications of a weak economy. As for the timing of the next move --it might be a while, there is no hurry to do anything.

Friday, September 01, 2006

Employment Takes The Fed Out, Business Week Takes Out Housing

After dipping a bit in April and May, nonfarm employment added 128,000 seasonally adjusted workers. As key as this number is, remember Poole told us yesterday that it isn't one data point, June was revised up from 124,000 to 134,000 and July was raised to 121,000 from 113,000. August's employment number is also the three and the six month average. Right on target, as the Fed told us in early June, for trend growth at this level of resource utilization. A non-inflationary growth path if there ever was one.

The impact of this number means that Sep is officially off the boards (as if there ever should have been any doubt) and now Oct is wiped off as well. My reasoning is that the Fed, once again as Poole told us, reacts to strings of data that paint a story in line with other data. The data the Fed is most sensitive to is employment -- after all, that is one of their two missions. No matter what the Sep data show in October, it is not going to cause the Fed to react. I leave out, of course, the unforeseen random event that could crater the economy.

In the past few trading days, however, the market has been pushing up the odds of an ease. After the data came out, there was a brief selloff that was effectively pulling those odds back to zero. But neither is the market to be daunted by one data point. So when the 7% drop in pending homes drop (month-over-month) came out, the market rallied the ease scenario back into the price structure for 2007. In creating this outlook for weak growth based on weak housing, the market obviously discounts the 17,000 construction jobs added in August v 5,000 in July and after shedding 6,000 in May and June combined. Perhaps Poole was right in his q&a yesterday when he noted that other areas of construction, namely nonresidential, was fine and there is an overblown importance given to housing.

Based on inter-month spreads in the Federal funds futures contracts, the market is pricing in an approximate 30% chance of the Fed easing in January. From now to year end, the market is giving about a 60% chance that the Fed does nothing and thus a 40% chance, equally divided, that the Fed does something. Right where the Fed wants us -- smack in the middle recognizing the equal probability of an ease or a tightening.

When the Fed-speakers address current market expectations, I believe they are talking about the ease priced in for next year. By my calculations, the market is giving 50/50 odds that the Fed will cumulatively drop the funds rate 100 basis points in 2007. The market has kept this view even though employment is rising apace, income is up, gas prices are down, and the dollar is weaker (helps capex. The only reason I can surmise is the singular focus on housing. Not just the knock-off effect of reduced construction and rising inventories of unsold homes, but also the ticking time bomb of the impact of rising rates and falling home prices on various exotic mortgages.

This week Business Week has the following cover story:

Now we can rest assured that everything is fine. Will all due respect to the hard working folk at Business Week, their covers have been a contratrend indicator for years.

I still hold that the biggest risk in the fixed-income market is the stubborn view that the economy will slow and the Fed will ease. Perhaps with the end of summer, cooler temperatures will bring about more rational reasoning.

The impact of this number means that Sep is officially off the boards (as if there ever should have been any doubt) and now Oct is wiped off as well. My reasoning is that the Fed, once again as Poole told us, reacts to strings of data that paint a story in line with other data. The data the Fed is most sensitive to is employment -- after all, that is one of their two missions. No matter what the Sep data show in October, it is not going to cause the Fed to react. I leave out, of course, the unforeseen random event that could crater the economy.

In the past few trading days, however, the market has been pushing up the odds of an ease. After the data came out, there was a brief selloff that was effectively pulling those odds back to zero. But neither is the market to be daunted by one data point. So when the 7% drop in pending homes drop (month-over-month) came out, the market rallied the ease scenario back into the price structure for 2007. In creating this outlook for weak growth based on weak housing, the market obviously discounts the 17,000 construction jobs added in August v 5,000 in July and after shedding 6,000 in May and June combined. Perhaps Poole was right in his q&a yesterday when he noted that other areas of construction, namely nonresidential, was fine and there is an overblown importance given to housing.

Based on inter-month spreads in the Federal funds futures contracts, the market is pricing in an approximate 30% chance of the Fed easing in January. From now to year end, the market is giving about a 60% chance that the Fed does nothing and thus a 40% chance, equally divided, that the Fed does something. Right where the Fed wants us -- smack in the middle recognizing the equal probability of an ease or a tightening.

When the Fed-speakers address current market expectations, I believe they are talking about the ease priced in for next year. By my calculations, the market is giving 50/50 odds that the Fed will cumulatively drop the funds rate 100 basis points in 2007. The market has kept this view even though employment is rising apace, income is up, gas prices are down, and the dollar is weaker (helps capex. The only reason I can surmise is the singular focus on housing. Not just the knock-off effect of reduced construction and rising inventories of unsold homes, but also the ticking time bomb of the impact of rising rates and falling home prices on various exotic mortgages.

This week Business Week has the following cover story:

Now we can rest assured that everything is fine. Will all due respect to the hard working folk at Business Week, their covers have been a contratrend indicator for years.

I still hold that the biggest risk in the fixed-income market is the stubborn view that the economy will slow and the Fed will ease. Perhaps with the end of summer, cooler temperatures will bring about more rational reasoning.

Subscribe to:

Comments (Atom)